In recent days there have been reports of some significant price hikes in the retail aftermarket as hard drives are being used for new applications like crypto mining…could you discuss how demand in the channel may be impacting your factory utilization and lead times across your customer base?

CEO:

…the customers in the channel are varied and important to us, so we always budget enough capacity to make sure that we’re servicing the channels well. We do see the uptick in demand that you’re referring to; we’re watching the different trends that are causing it, some of them are really interesting vibrant trends, and we love that!

What I would say is that it’s a little early in this to know how prolonged it will be, I think we’re even early in this quarter, so it’s really hard to know exactly what the distribution channel reaction is going to be. I also think that getting people things immediately is a problem in the world today…even if it came out of the back of our factory, getting it around the world to that channel location might be a problem…

ARMCHAIR COMMENTARY

Disclosure: I’m already long $STX. Don’t take investment advice from Internet posts, etc.

Seagate’s stock might be a picks-and-shovels play on Chia going to the moon, if you believe in that. As they expect to ship roughly 500 EB of capacity this year, you have to be wildly Chia-maximalist to make a case on fundamentals alone; but, the current speculative environment lends itself to the wild things. If this summer CNBC were to haul Bram or Gene on, and/or some configuration of Elon/Mark/Cathy/Michael/TylerCameron/Raoul take notice…who knows?

On the other hand, Seagate’s downside risks, relative to the tech device sector in general, seem manageable – with solid financials, and a healthy outlook for the next few years.

Salient background from my personal research:

Seagate $STX, Western Digital $WDC, and Toshiba (Tokyo-listed) supply ~all of the spinning HDD market, roughly 40/40/20 respectively

STX is all-in on HDDs, while WDC is spread ~50/50 with flash

WDC’s earnings and balance sheet are somewhat stressed, owing to their heavy investments to compete in flash, an obvious growth area

STX on the other hand has been milking the HDD cow, with healthy earnings, steady dividends, and stock buybacks, and doesn’t have a real flash story

That makes some analysts pessimistic, due to the likelihood of flash further closing the $/TB gap on a 5-year horizon. Morningstar has an outright Sell rating, mainly for this reason.

STX themselves categorize PC and retail HDDs as “Legacy” markets, with revenue erosion expected to continue (outpaced, hopefully, by mass storage demands in cloud & edge)

Their 22 trailing P/E on $19.5B cap, is moderate for the sector. Comparables:

Upside: Micron (31) and NetApp (28)

Downside: Intel (13)

Moon: NVIDIA (86)

Since 3/17/2020 STX rose about as much as QQQ; although it underperformed for most of that time, relatively outperforming only in the last few months (hmm…)

They own a small slice of Ripple Labs, perhaps inducing some existing correlation to crypto; probably just a few percentage points though

Could the stock get revalued upwards later this year, based on the emergence of a crypto-hyped use case for HDDs, with potential to (i) re-energize the PC and retail markets and (ii) rationalize enterprise & hyperscalers to further overprovision and pull forward refresh cycles? On the other hand, are there huge downside risks not already priced in? You decide!

Let’s say you knew that there’s a good chance that western digital and seagate were going to pop in a week to a month time frame, what kind of high risk option would you buy?

Earlier this week, the setup in $STX made me comfortable enough to simply buy shares in an IRA (OMG, who still does that!? ) to hold through EOY or so. I personally don’t perceive it having much risk in excess of the typical tech stock, in that timeframe.

There’s a nice candle up to 89 today with the strong earnings, but if you suppose for example the P/E could rise to near Micron’s, that’d take it to 120ish. My market data suggests somebody (not me or anybody I know!) bought a bunch of January 105 calls today, 1,470 contracts which would pay out a cool $1.1M if it did hit 120 in that timeframe, with 400K risked.

I still need to do more research on playing the flash side with Western or Micron. Seagate is very simple to analyze by comparison, since they’re basically all-in on one product line that only has two other suppliers.

I like this trade but I don’t think the risk / reward is quite there with that way of doing it. I’d go much shorter expiry options as, once (if) the equity market figures out Chia and its impact on storage manufacturers the prices will really pop quickly in anticipation of future earnings.

Yea I have no way to know exactly where those contracts traded; the bet might have been more like 4:1 or a little better, if it was in the first hour last Friday.

Since $STX is a mature profitable business, not some garbage meme stock, I’m personally happy to own shares the old-fashioned way; but, we’ve each got to choose trades sufficiently leveraged for [our] Personal Risk Tolerance

Question I’m noodling on to think about the fundamentals – is storage right now more like N-95 masks or TP, circa March 2020?

N-95 masks: it was a boring product with predictable global customer base, then suddenly demand spiked to infinity, and remains elevated for years and to some extent, permanently

Toilet paper: rumors of shortages became self-fulfilling prophecies as supply chains took time to reorient and redirect e.g. from offices to homes. However, this settled down within a few months, because the actual consumption per person didn’t structurally increase, the purchasing demand just shifted in space and time.

To be clear though, I think $STX and related stonks could be in for a ride, somewhat regardless of the long-term fundamentals…

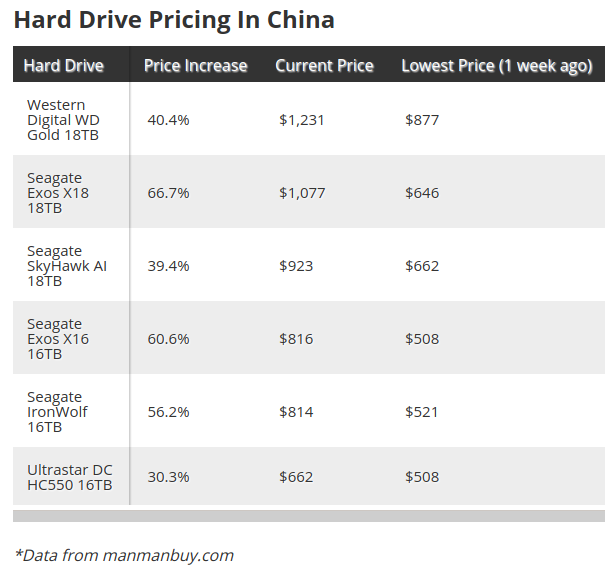

Oh that’s in China (the picture) haha - I glanced at it, freaked out, checked few websites and i saw similar prices (old) and I was confused for a moment haha. I am in the US and I didn’t see any increase in prices, at least nothing major as above.

The big increase here might happen if on 3rd of May XCH is worth a lot and hype is created and people jump on board. So your comparison to n95/tp is very good - as the TP especially was due to the hype/fomo

This is the key. In a weird way, you can buy options on $XCH right now (sort of). Just buy 7th or 14th May expiry call options on the manufacturers. That’s what I’m going to do tomorrow morning, anyway. If $XCH goes to the moon then the prices of the underlying should shoot up. If not, then only the option premium lost. This is definitely not financial advice!

The STX 21-May 99 strike calls I bought on Monday are up well over 100% Only regret (of course!) is not buying more.

I am not sure how much of that was Chia and how much of that was just positive momentum off the back of earnings. The underlying is up about 15% this week it looks.

WDC Q3 2021 earnings call transcript and slides. My highlights below.

Hard drive revenue was $2 billion, up 3% sequentially and down 7% year-over-year. On a sequential basis, total hard drive exabyte shipments increased by 7%, while the average price per hard drive increased 14% to $82.

We have completed qualifications for our energy-assisted drives with nearly all our cloud and enterprise customers, including all the cloud titans and expect an aggressive ramp of our 18-terabyte hard drives. Building on this success, we’ve entered into long-term agreements with a number of our cloud titans for 18-terabyte drives.

Finally, in February, we revealed BiCS6, our next-generation flash device, based on 162 layer and CuA technology, developed in partnership with Kioxia as part of our long-standing successful joint venture, BiCS6 features numerous architectural advancements, including improved lateral scaling, which allows us to deliver this high-performing product at an optimal cost.

To date, we have been able to largely mitigate the impact of the industry-wide semiconductor component shortages through proactive supply chain management. We are, however, experiencing tightness in controllers as well as flash, which could limit potential upside in the future.

And we definitely are carrying a little more inventory than we normally would, particularly on the hard drive side because of the tightness on controllers. And also, frankly, because of the logistics costs associated with COVID-19, we’re putting more products on the ocean and not in the air. So it’s definitely having an impact in terms of working capital in that respect.

Seagate has been making drives for more than four decades, and investors have been skeptical throughout. At various times, the business has been criticized as too competitive, commoditized, wildly cyclical, and obsolete. Those worries have made Seagate one of the cheapest stocks in tech land, which still holds true today.

Seagate could even be a play on cryptocurrency, given the recent surge in demand for drives tied to Chia, a new cryptocurrency started by Bram Cohen, the creator of BitTorrent, a communications protocol that eased the sharing of large files.

Chia relies on storage, instead of processing power, to mine new currency. (Chia uses the term “farm,” rather than “mine.”)

Northland Capital Markets analyst Gus Richard says Chia farmers have triggered a spike in retail sales for high-capacity drives, doubling prices in some Asian markets. If that continues, drive supplies would tighten and prices would rise.

Based on its forward earnings multiple, Seagate is trading at a 50%-plus discount to the Nasdaq Composite index. And it fetches less than two times estimated sales, well below the seven times average for the cloud stocks in the Global X Cloud Computing ETF (CLOU).

Seagate might now be the world’s cheapest bet on the cloud.

He estimates that Chia farmers have already purchased about 10 exabytes of hard-drive capacity. To put that in perspective, he said, total monthly sales of enterprise-class drives has been running about 80 exabytes.

The analyst said hard-drive prices in the U.S. market rose 7.4% from the week ended April 25 through the week ended May 2—the largest weekly increase since at least 2015. So far this quarter, average selling prices are up 8.2%, a record…

The analyst’s thesis is that the spike in demand will fade after the second quarter – but he also raised the question of what happens if it doesn’t. The total value of Chia created to date is about $500 million, but the Bitcoin market is about 2,000 times that, he said…

The cryptocurrency world’s hot new thing is Chia, a new digital currency dreamed up by Bram Cohen, also the founder of the wildly popular file-download service BitTorrent. In one of the weirdest twists of this particular craze, China’s so-called cryptocurrency farmers are driving a mammoth rally in shares of disk-drive makers Seagate and Western Digital.

Over the last three trading days, shares of Western Digital (ticker: WDC) and Seagate (STX) have rallied 24% and 19%, respectively. The rally accelerated on Friday after Morgan Stanley analyst Joseph Moore noted that a huge increase in demand for high capacity disk-drives was driving up prices and creating shortages.

Thanks for sharing

Thanks for sharing ) to hold through EOY or so. I personally don’t perceive it having much risk in excess of the typical tech stock, in that timeframe.

) to hold through EOY or so. I personally don’t perceive it having much risk in excess of the typical tech stock, in that timeframe.

Only regret (of course!) is not buying more.

Only regret (of course!) is not buying more.